![]() |

|![]()

1.Objectives

To appoint the authority, accountabilities, and responsibilities of the Audit Committee in compliance and supervise the performance of management in the areas of internal control, as well as financial report of the company to be systematically, constantly, and effectively in accordance with financial policy and regulations for the highest effectiveness complying to Audit policy.

2.Composition

Audit Committee of the company shall consist of:

2.1.At least 3 persons: which consist of one chairperson, and at least 2 directors designated by the resolution of the Board of Directors meeting or Annual General Meeting of Shareholders.

2.2.The Audit Committee may assign any employee in the company to be the secretary of the Audit committee

2.3.The Audit Committee may assign any employee in the company or external person to be the advisory of the Committee

3.Qualification

3.1.The members of the committee shall be a director of the company

3.2.The members of the committee shall liberally and truthfully perform assignments, give opinions, and report accomplishment as appointed by the Board of Directors. The committee members shall also be honest, and not be under control of the management, major shareholders, or any other persons related to those people.

3.3.The members of the committee shall sufficiently devote and give opinions to performing as the Committee.

3.4.The members of the committee shall have understanding company business, have good business management and abilities to analyze the problems as well as have skills to make a good decision.

3.5.At least one of the Audit Committee shall have understanding, knowledge or experience sufficiently to review and accept the financial report as well as general risk management.

4.Term of Position

4.1.Members of the Audit Committee shall hold the position 2 years for each term. After the term is expired, the members could be re-nominated.

4.2.If the member would like to resign from the Committee before the term ended, such member shall inform the Board of Directors 1 month in advance, so that the Board of Directors would nominate other qualified director to replace the resigned member.

4.3.The Committee member shall be out of position when not being company directors, term ended, resign, the Board of Director’s resolution or no specified qualification as stated by law

4.4.In case that any position of the Committee is unoccupied because of other reasons besides the term ended, the Board of Directors shall nominated qualified director replacing that position within 3 months since the date of vacancy.

5.Authority Accountabilities and Responsibilities

The Audit Committee has authority accountabilities and responsibilities as follows:

5.1.Review the financial report of the company to be integral and authentic.

5.2.Review the financial auditor performance, consider the selection, and propose the nomination and the compensation of the auditor to the Board of Directors.

5.3.To appoint and review the Audit Committee Charter and Internal Audit Charter at least once a year and propose to the Board of Directors for approval.

5.4.Consider and approve the internal audit plan, the policy, procedure, and audit process for Credit Scoring Preparation and Disclosure, manual of the internal audit department, budget and human resources of the internal audit department.

5.5.Support and supervise the independence of the internal audit department.

5.6.Consider and agreed the appointment removal rotation change positions or termination the Head of Internal Audit and propose to the Board of Directors for approval.

5.7.Consider and approval the recruitment and the evaluation of performance of the officer or employee in the Internal Audit Department.

5.8.Oversee the selection of external informational technology independent auditor or specialized advisor for auditing and advising in accordance with the agreement of the Board of Directors

5.9.Supervise the internal control and internal audit to be adequate, appropriate, and effective

5.10.Consider and monitor the improvement according to the suggestions and guidance related to internal control and risk management, which given by external auditor, internal auditor and the regulators.

5.11.Supervise the company to comply with the rules and regulations and also any related of credit information laws.

5.12.Prepare the annual report of the Audit Committee, which signed by the chairperson of the Audit Committee, and propose to the Board of Directors.

5.13.May request meeting with the management, supervisor, or related officer to explain or give information in the Audit Committee meeting, or request to send the related document as deem appropriate.

5.14.If any following actions significantly affect the financial status or performance of the company, the Audit Committee shall report to the Board of Directors for further improvement by the suitable time.

(1) Transaction that causes the conflict of interest

(2) Fraud or any significant irregular events or problems in the internal control system

(3) The violation of Credit Information Law

5.15.Any tasks or duties assigned by the Board of Directors

6.The meeting

6.1.The Audit Committee shall hold the Committee meeting at least once in a quarter.

6.2.The committee’s member should attend the meeting no less than half of the Committee to be called the quorum

6.3.The resolution of the meeting would be based on the majority vote of the Audit Committee. If the vote is equivalent, the Chairpersonof the Audit Committee would finalize the decision

6.4.While seeking for a director to replace the vacant position, at least another 2 directors in the Audit Committee can hold the meeting and continue any work according to the authority, accountabilities and responsibilities of the Audit Committee The Audit Committee may invite related person such as directors of the company, management, officer, and/or the subsidiary or holding companies and financial auditor to clarify or answer the questions.

7.Reporting

7.1.The Audit Committee shall report the summary of the meeting and/or the performance of the Audit Committee to the Board of Directors at least once in a quarter.

7.2.In the annual audit report of the Audit Committee should indicate intention, objectives, responsibilities, and mission or activities of the Audit Committee in the past year. Also, the Audit Committee should give suggestion of further improvement to the Board of Directors, and give opinion on the internal control system as well as the financial report.

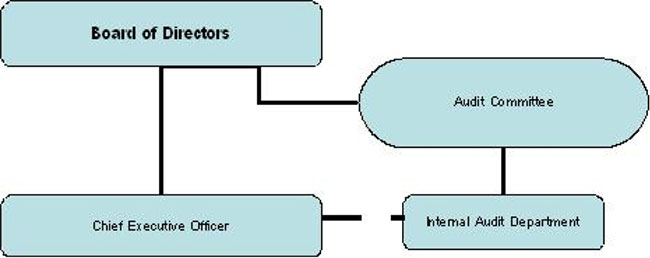

8.Organizational Structure

Adoption of Charter

The Audit Committee endorsed this charter on December 23, 2015. This Charter has been enacted since 21 March 2016 by the approval of the Board of Directors in the 3/2016 meeting dated 21 March 2016.

Mr.Ekniti Nitithanprapas

Chairman of the Board of Director